WE BELIEVE ININNOVATIONADAPTABILITYSAFETYRELATIONSHIPSQUALITY

Customer-specific construction solutions — from initial concept to final completion with precision, quality, and efficiency.

BUILDING DREAMS

INTO REALITY

Nupas Ltd is a consortium of internationally acclaimed design professionals. A multi-disciplinary organization that's responsive to the challenges of a dynamic and changing society, committed to improving man's environment within the context of continuous social and technological changes.

Our solutions to our clients' goals emerge from a process that includes the client as a participant rather than as an observer. We bring over thirty years of professional practice across a wide variety of building types.

Learn More About Us

Featured Projects

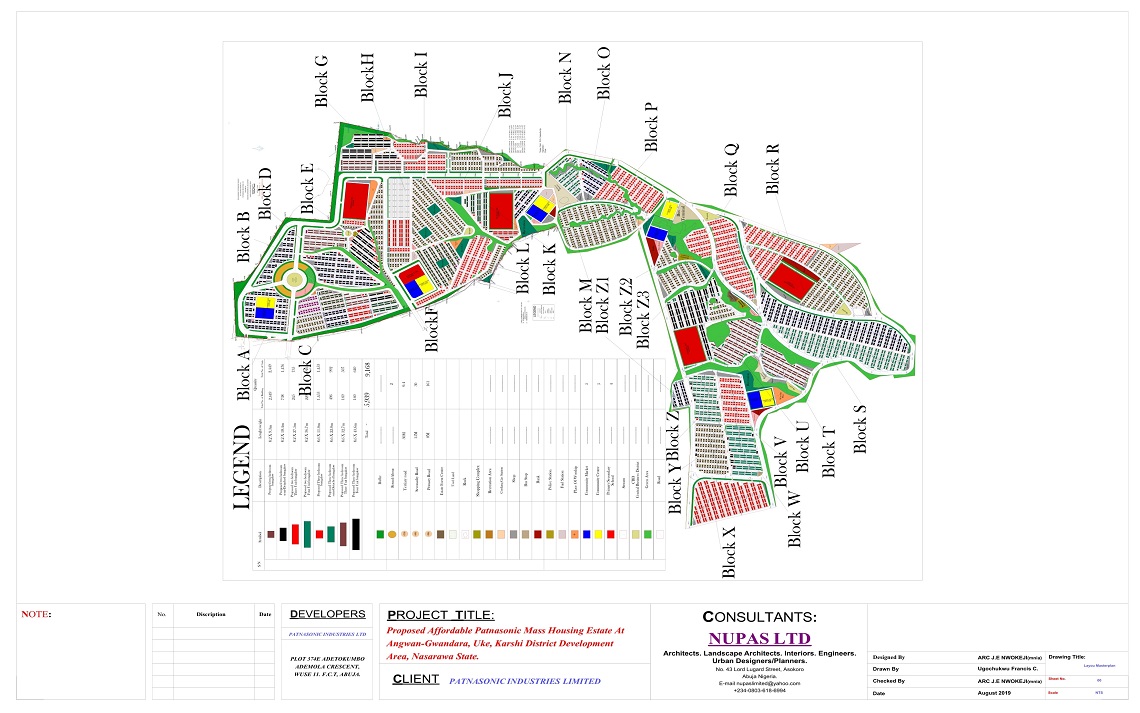

Patnasonic Mass Housing

A large-scale mass housing estate designed for modern living with sustainable building practices.

Abuja, NG

3D Duplex Concept

Innovative 3D-printed duplex concept pushing the boundaries of construction technology.

Lagos, NG

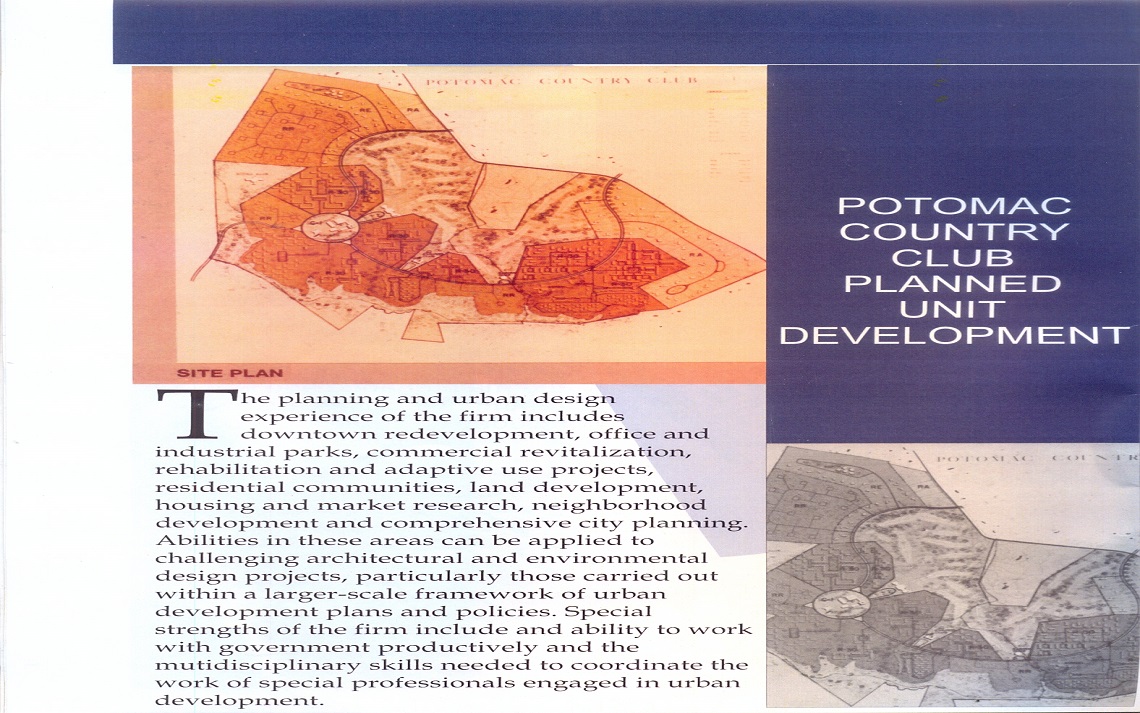

Potomac Country Club

Premium country club facility featuring world-class amenities and elegant design.

Abuja, NG

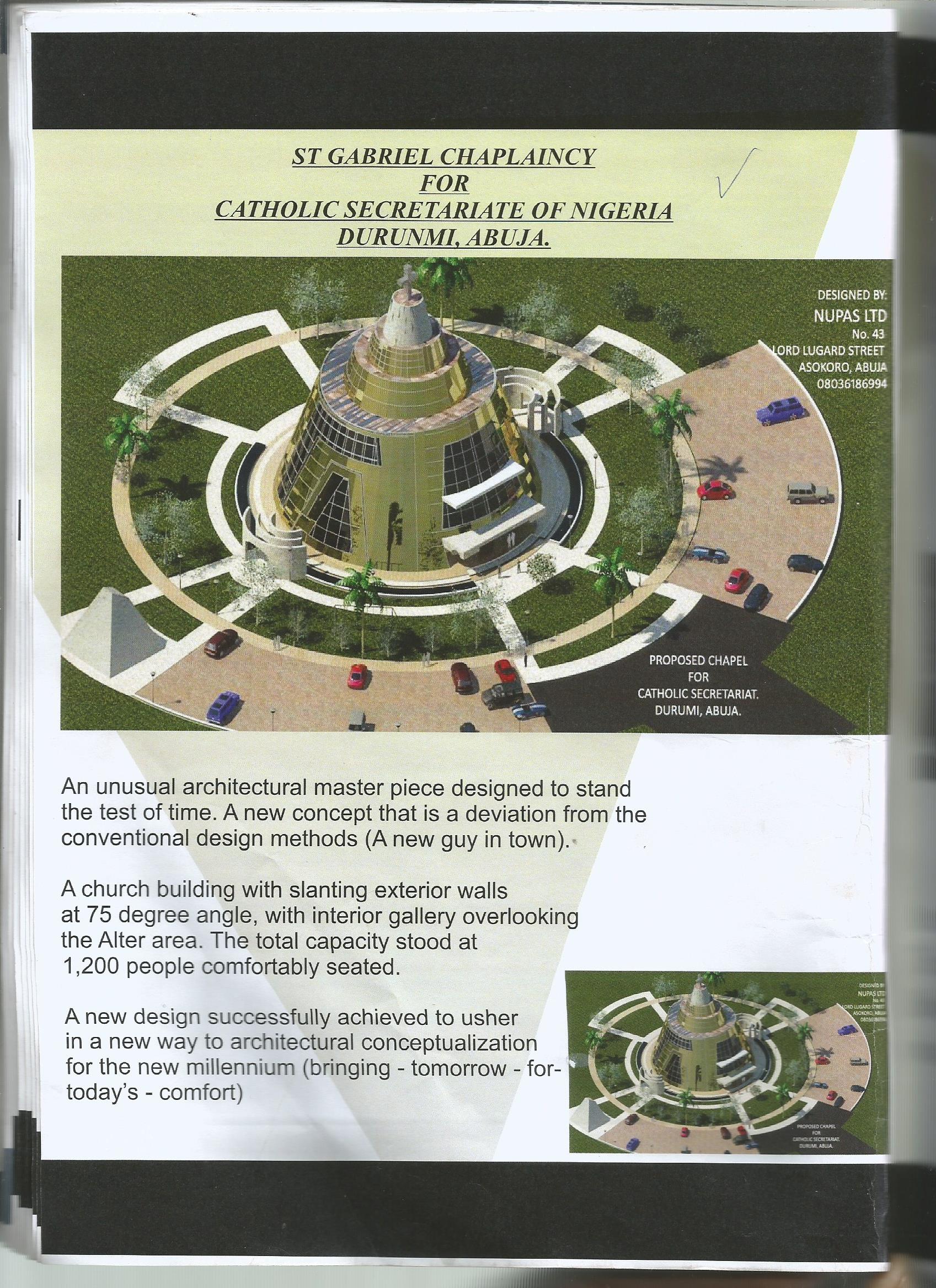

Saint Martins 3D

State-of-the-art institutional building with modern architectural elements.

Enugu, NG

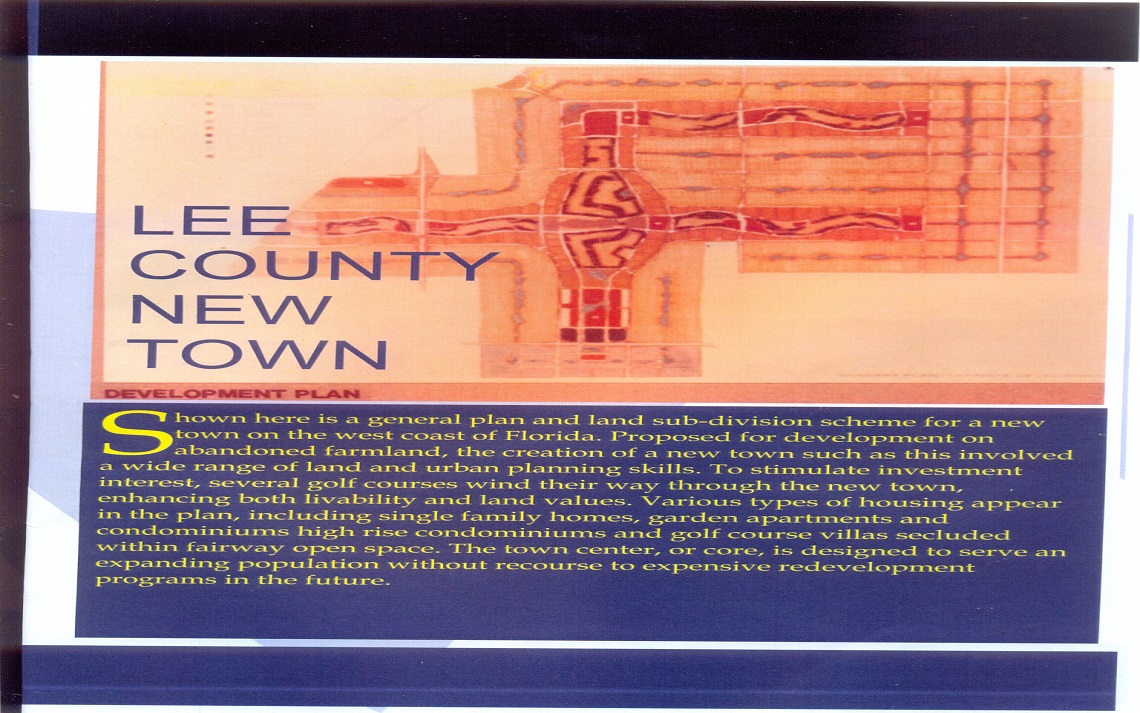

Lee County New Town

Comprehensive urban development project creating a vibrant new community.

Owerri, NG

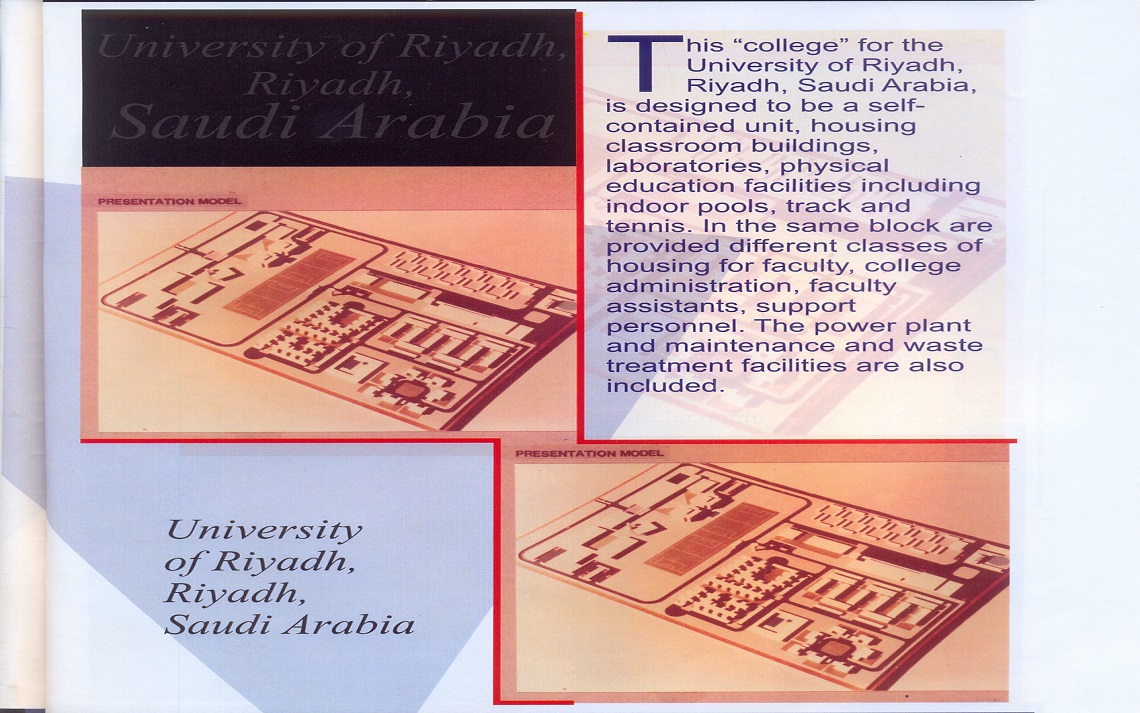

University of Riyadh

Modern educational campus designed for world-class learning experiences.

Riyadh, SA

The Latest News & Press

Delivering Excellence in Residential Architecture

A client shares their experience with Nupas Ltd on a bespoke residential project in Abuja.

Read MoreTransforming Urban Spaces Through Innovative Planning

How Nupas Ltd delivered a comprehensive urban planning solution that revitalised a community.

Read MoreEngineering Precision on a Large-Scale Commercial Project

A corporate client attests to Nupas Ltd's engineering expertise on a major commercial development.

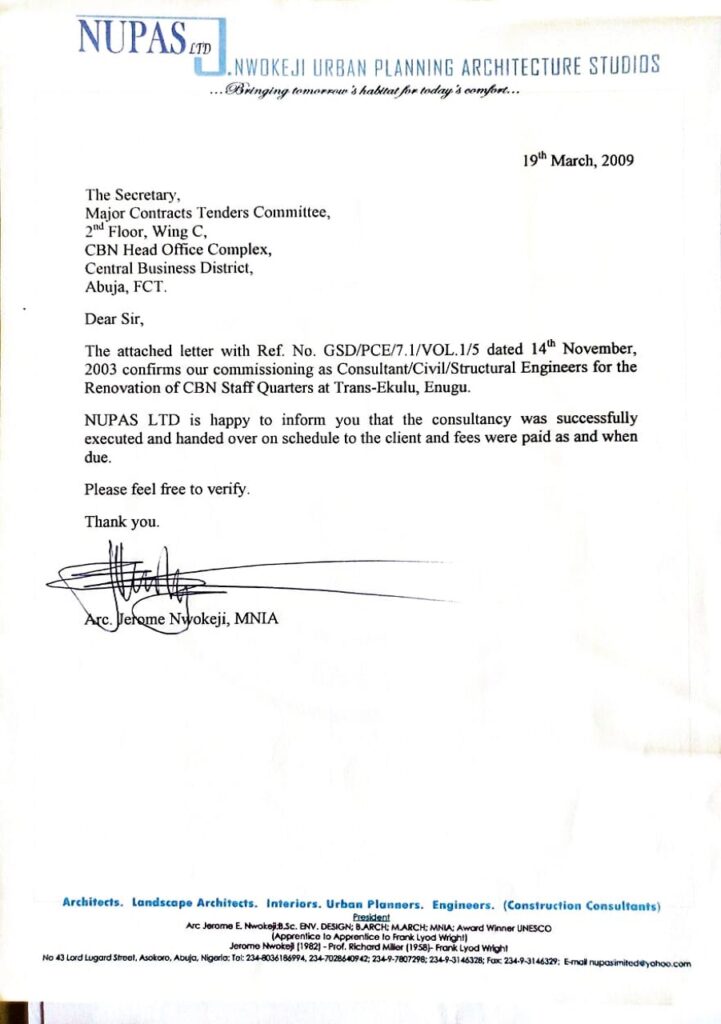

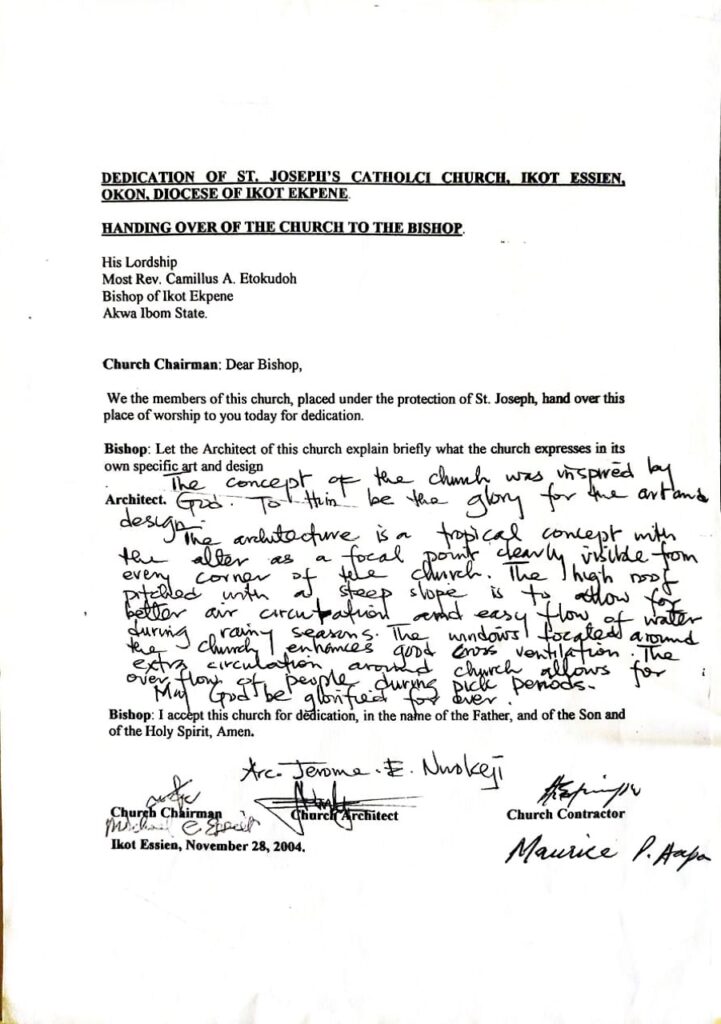

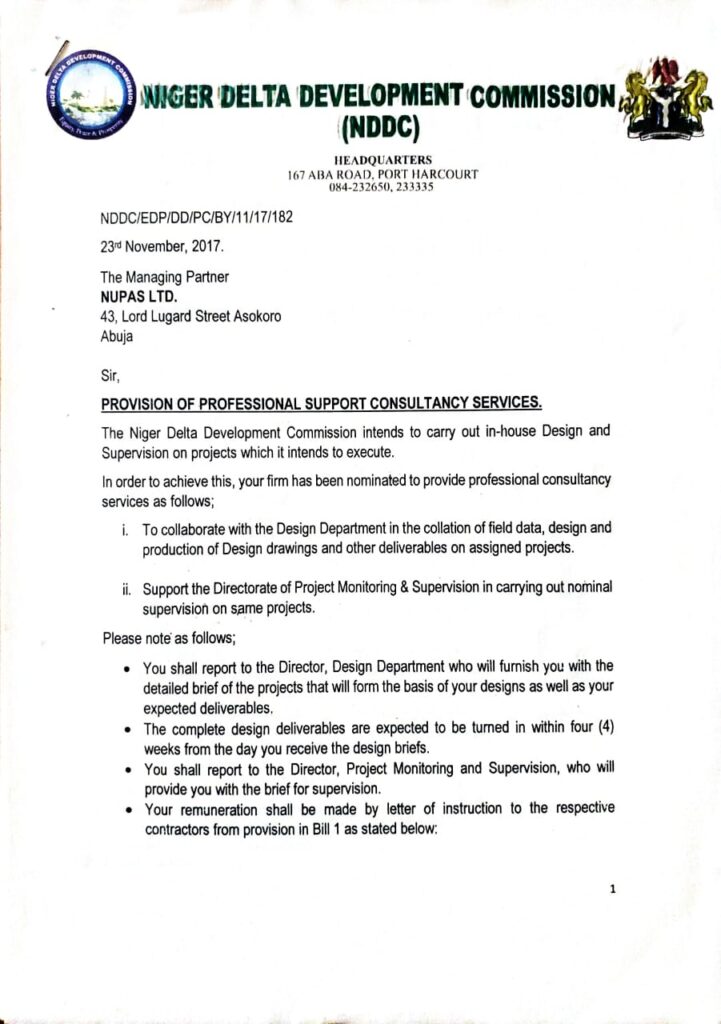

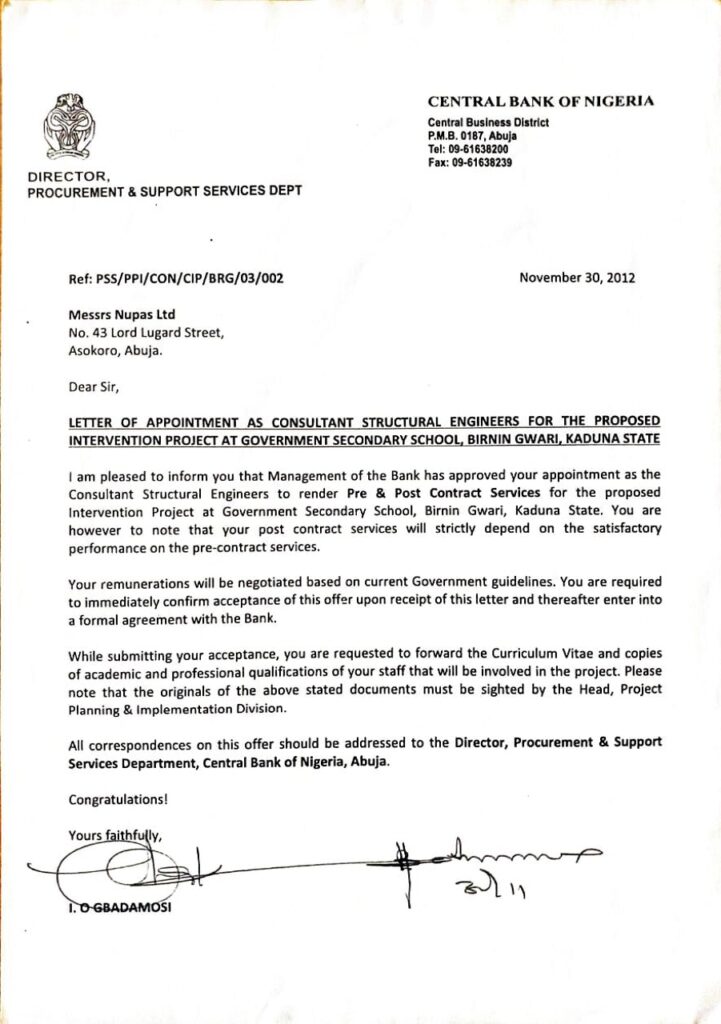

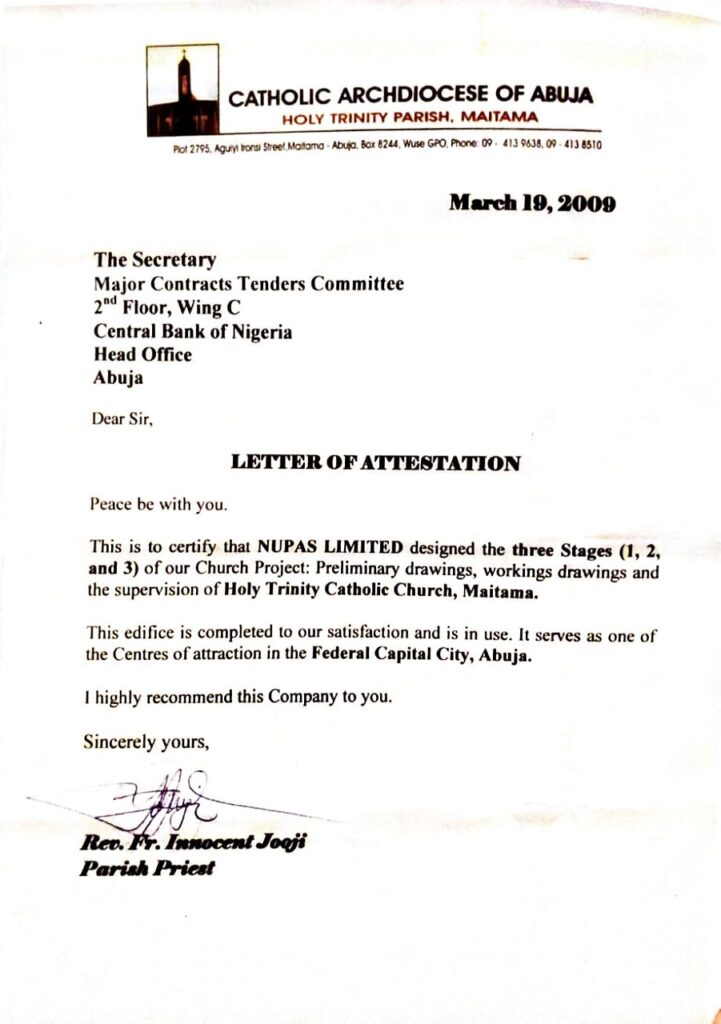

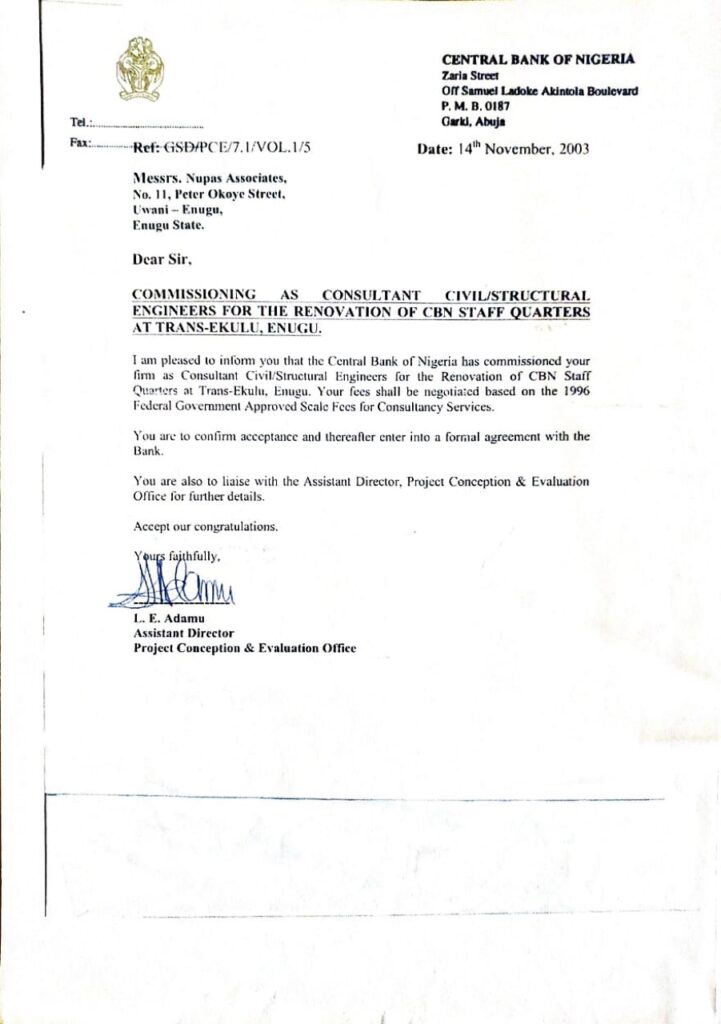

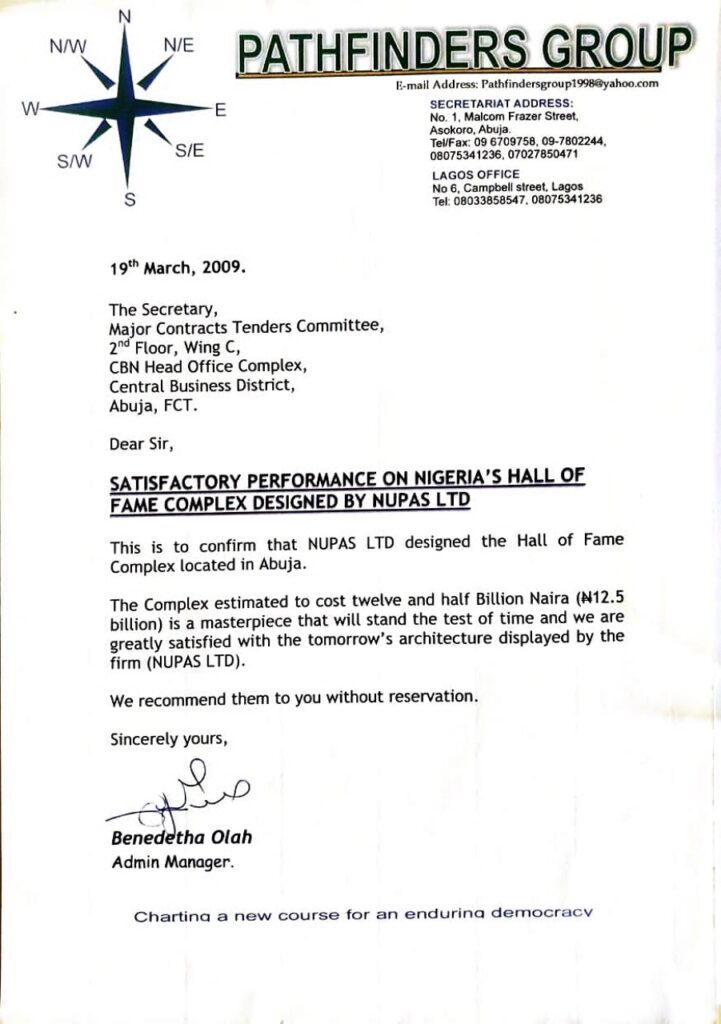

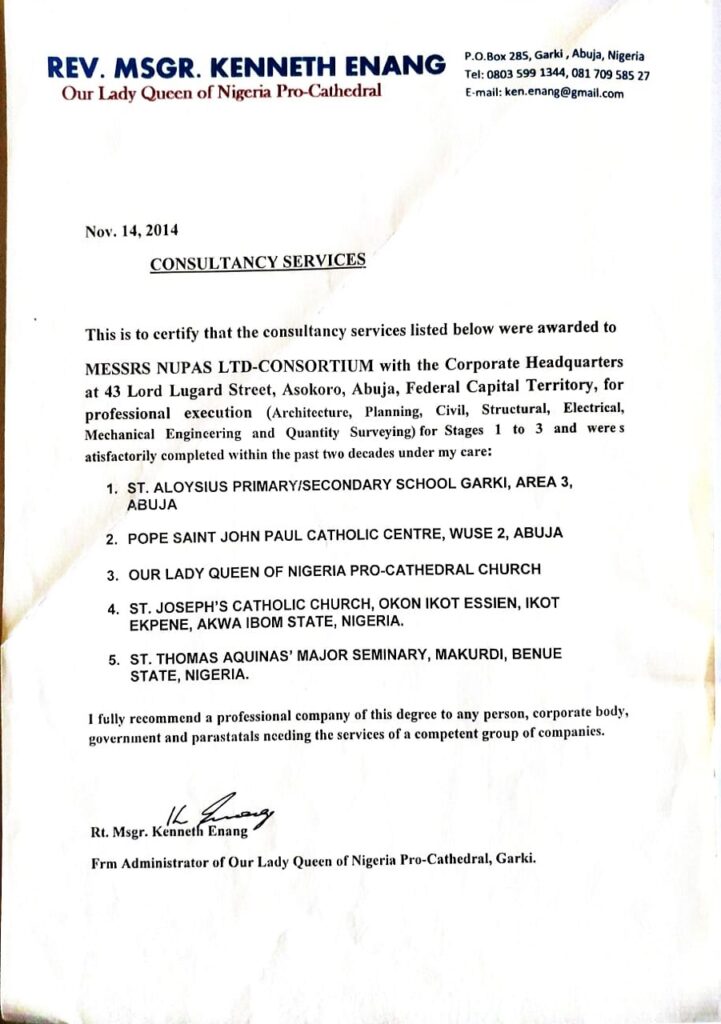

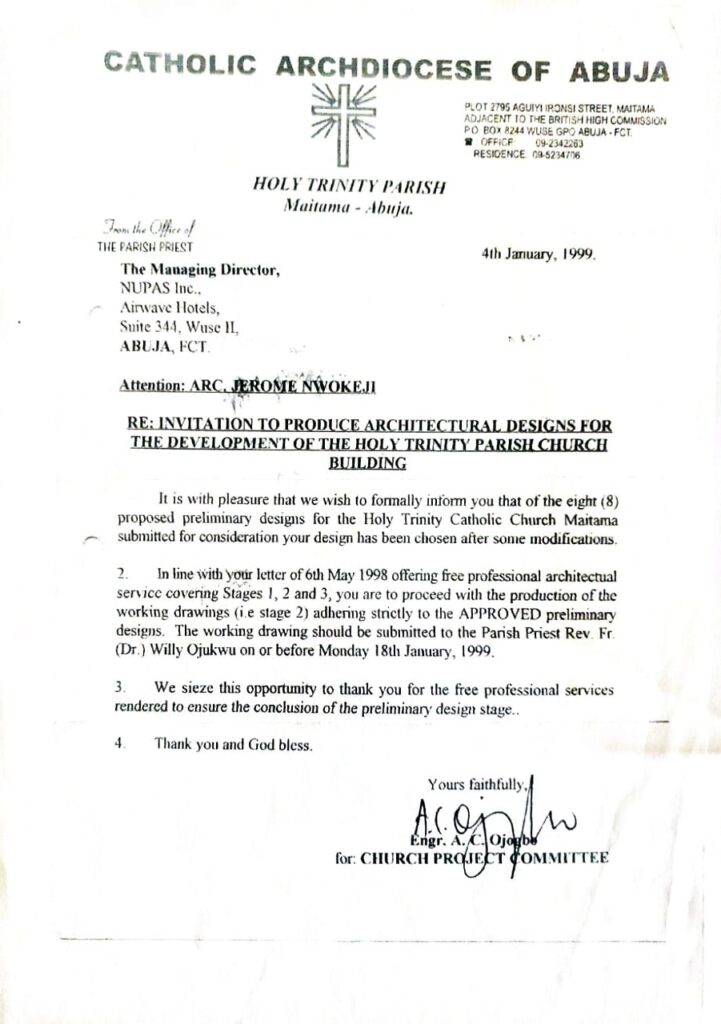

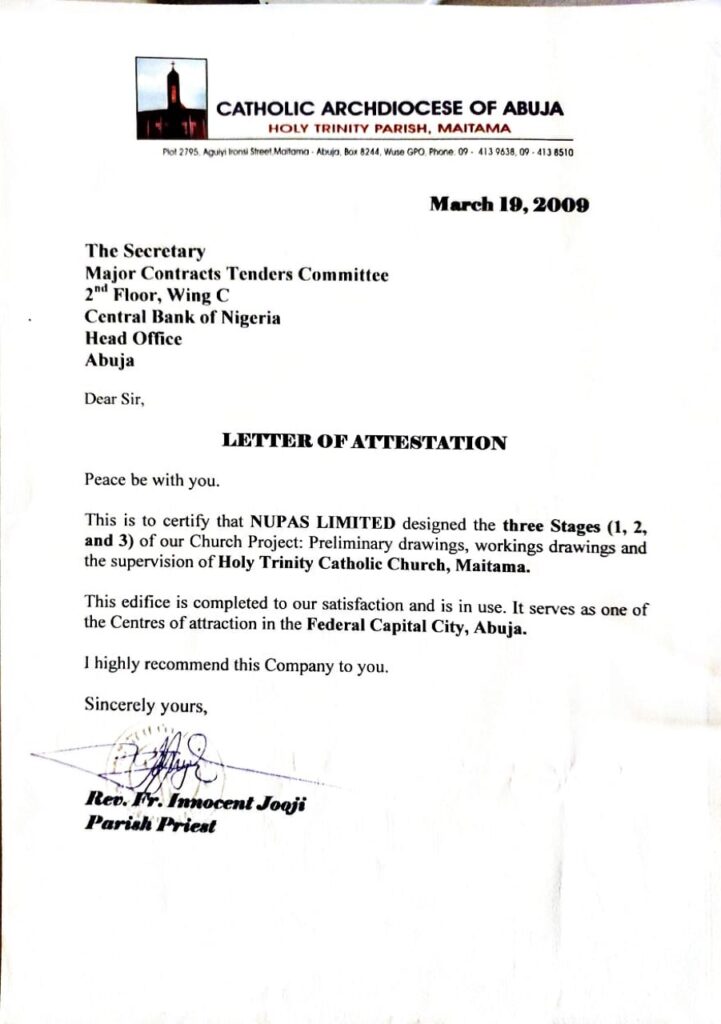

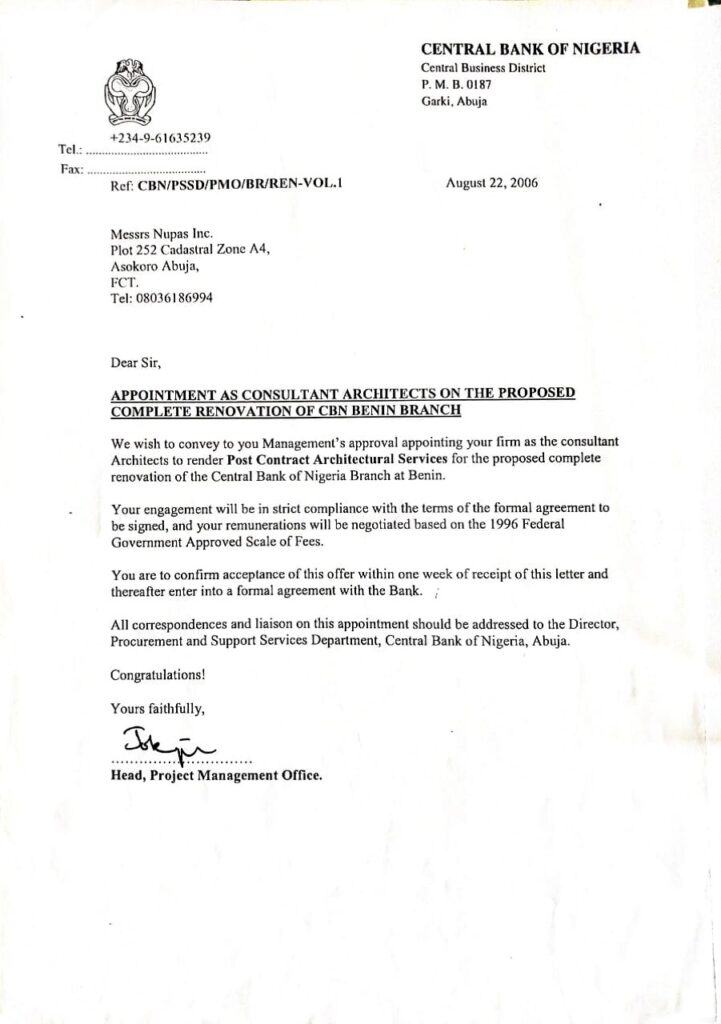

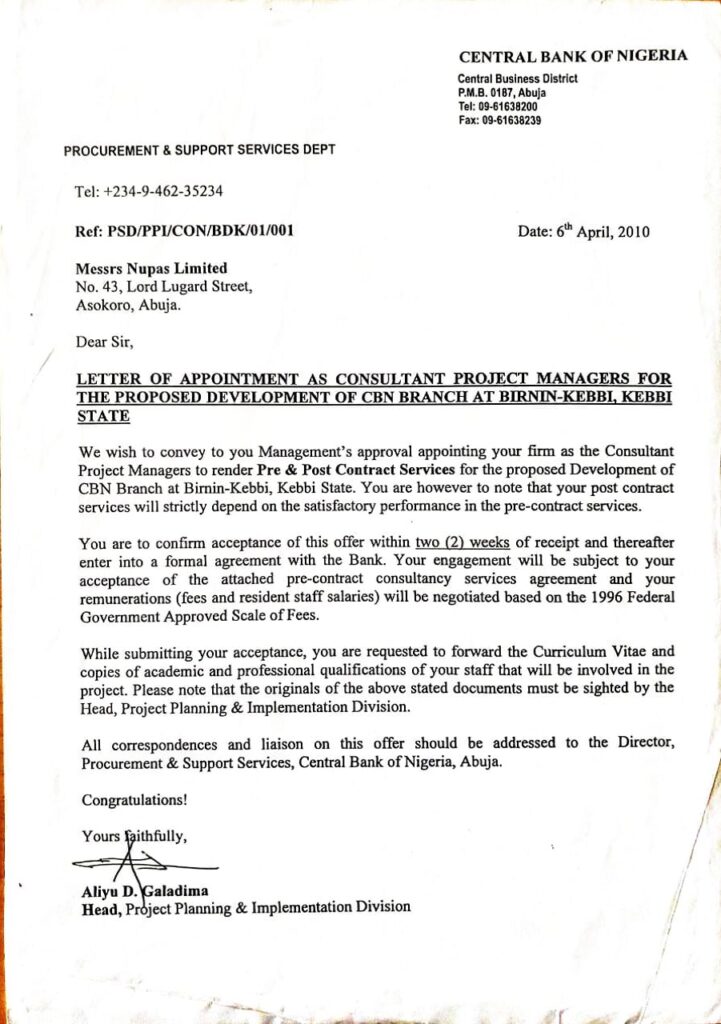

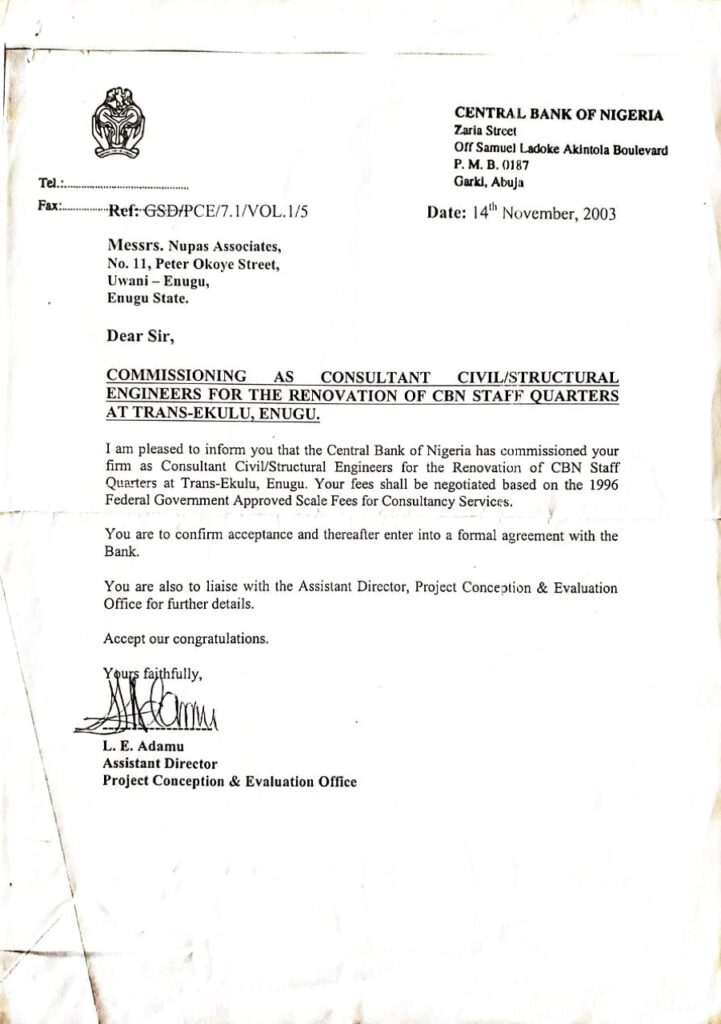

Read MoreClient Attestations

Letters of attestation from our valued clients — a testament to our commitment to excellence.